Taxes for real estate are a big part of the financial planning process when selling or investing in property. They can vary greatly from one state or another, so it is important that you understand your local laws to ensure that your investment is properly taxed.

Capital gains as well as property taxes are the biggest taxes to be worried about. You may also need to be aware of the transfer taxes that might apply to real estate transactions. These include state and local fees, as well as a transfer tax that is levied by a city or county.

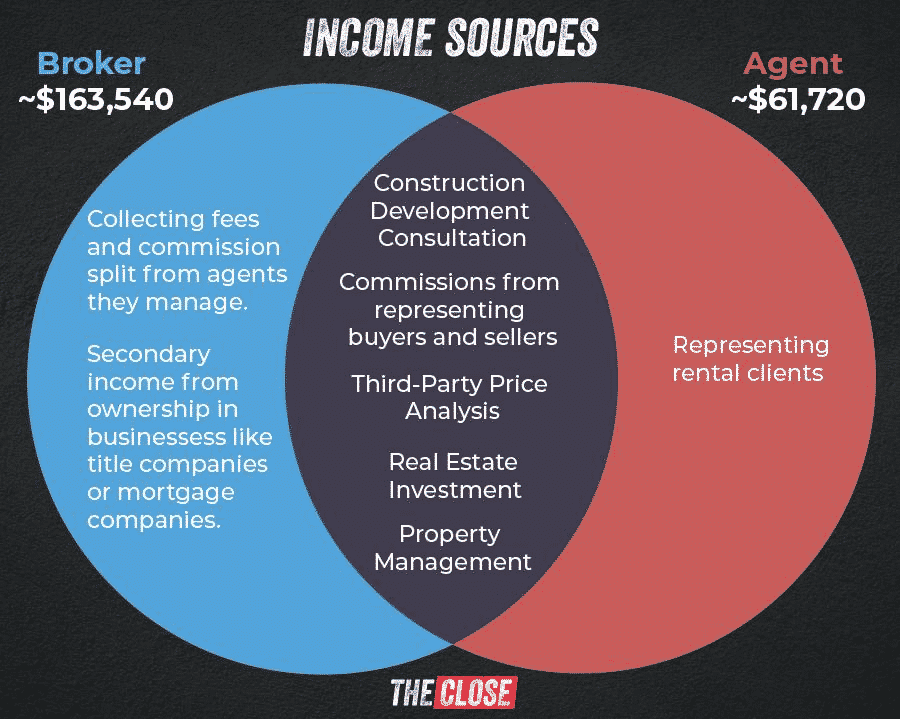

Real estate agents who are self-employed must file their own tax returns. It is important for them to keep track of the business expenses and any potential tax deductions throughout each year.

An agent can deduct office costs, equipment, and insurance. They are also allowed to deduct advertising and marketing costs, such as the development of their name or promotion of their listing.

While some real estate agents may be employees, others are independent contractors. Contractors pay their taxes themselves, while employees get their taxes automatically withheld.

What are some of the most common tax deductions that real estate agents receive?

Most people don't realize that real estate agents are eligible for a number of tax deductions. These include costs such as appraisal fees, advertising, insurance, and escrow. These fees can be deducted from commissions.

How do realty brokers pay their taxes?

A quarterly estimate of tax payments is required for self-employed agents. These estimates will help you calculate your tax liability and determine how much you need to pay. FlyFin offers a Quarterly Tax Calculator that can help you calculate your tax liability and determine how much to pay.

Some tax deductions may also be available to real estate agents. You can also deduct the cost of renewing your license or dues to other organizations. The cost of your Errors or Omission (E&O), Insurance can also be deducted from your commission as long as the broker is not withholding this cost.

Keep track of all expenses in your business and keep records throughout the fiscal year. This will help you save money on your tax bill. You can claim tax deductions and avoid penalties and fines by having well-organized accounts and documents.

As long as your vehicle is insured and registered, you can claim the cost of your vehicle used for business. Self-employed workers may also be eligible to deduct the cost for health insurance.

What are the best ways to pay taxes as a real estate agent?

You must keep track of your expenses as a self-employed realtor and file your taxes on the due date. Tax codes are always changing so it is crucial to stay on top of any potential changes that could impact your financial situation. You should also be able deduct all legitimate business expenses as long as they are not extraordinary and necessary to your business operations.

FAQ

How do you calculate your interest rate?

Market conditions impact the rates of interest. The average interest rate over the past week was 4.39%. Divide the length of your loan by the interest rates to calculate your interest rate. For example: If you finance $200,000 over 20 year at 5% per annum, your interest rates are 0.05 x 20% 1% which equals ten base points.

Is it possible to get a second mortgage?

Yes. However it is best to seek the advice of a professional to determine if you should apply. A second mortgage is often used to consolidate existing loans or to finance home improvement projects.

How can you tell if your house is worth selling?

It could be that your home has been priced incorrectly if you ask for a low asking price. If your asking price is significantly below the market value, there might not be enough interest. To learn more about current market conditions, you can download our free Home Value Report.

What amount should I save to buy a house?

It depends on the length of your stay. If you want to stay for at least five years, you must start saving now. If you plan to move in two years, you don't need to worry as much.

Do I need flood insurance

Flood Insurance covers flooding-related damages. Flood insurance helps protect your belongings and your mortgage payments. Find out more about flood insurance.

Statistics

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

External Links

How To

How to find real estate agents

Real estate agents play a vital role in the real estate market. They can sell properties and homes as well as provide property management and legal advice. Experience in the field, knowledge of the area, and communication skills will make a great real estate agent. To find a qualified professional, you should look at online reviews and ask friends and family for recommendations. You may also want to consider hiring a local realtor who specializes in your specific needs.

Realtors work with buyers and sellers of residential properties. A realtor's job is to help clients buy or sell their homes. As well as helping clients find the perfect home, realtors can also negotiate contracts, manage inspections and coordinate closing costs. Most realtors charge a commission fee based on the sale price of the property. Unless the transaction is completed, however some realtors may not charge any fees.

The National Association of Realtors(r), (NAR), has several types of licensed realtors. NAR membership is open to licensed realtors who pass a written test and pay fees. The course must be passed and the exam must be passed by certified realtors. NAR has established standards for accredited realtors.